Transfer pricing

This service is designed to calculate the arm’s length range of profitability set forth in article 105.8 of the Tax Code of the Russian Federation. To calculate the arm’s length range of profitability, it needs indicators on the financial statements of the compared companies for three (or two) calendar years preceding a year, when the analyzed transaction was completed (or preceding a calendar year during which the prices for analyzed transaction was set). The companies for comparison can be sorted by:

- industrial activity of organization (in accordance with OKVED code);

- place of registration of organization;

- net assets of organization as well as financial results of its activity;

- information about the size of shareholders’ stakes in organization and data about its subsidiaries and controlled organizations.

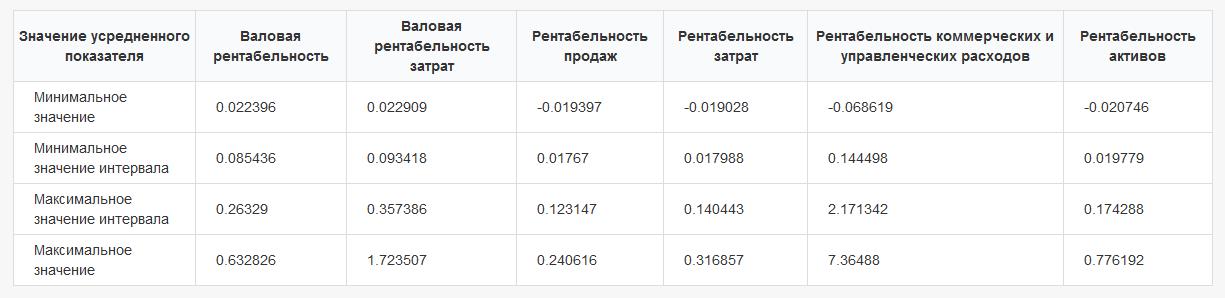

Organizations can be also sorted by particular parameters (such as required minimum revenue of an organization for the selected reporting period). The sorting results must include at least four compared organizations to calculate the arm’s length range of profitability. Once the compared companies are selected, the following profitability indicators of these companies will be calculated:

- gross margin;

- gross rate on costs;

- return on sales;

- rate on costs;

- return on commercial and administrative costs;

- return on assets.

Results obtained by calculation are used to determine the minimum and the maximum value of the arm’s length range of profitability in accordance with clause 4 of article 105.8 of the Tax Code of the Russian Federation.

Would you like to learn more about SKRIN services?

Send your request.